In 2026, scam exposure in the United States is no longer the most important story. Financial loss is.

Last year’s report was defined by volume: 68% of US respondents encountered scam attempts at least monthly, with younger adults disproportionately affected. Scam activity was persistently high, and digital fluency didn’t translate into cyber resilience.

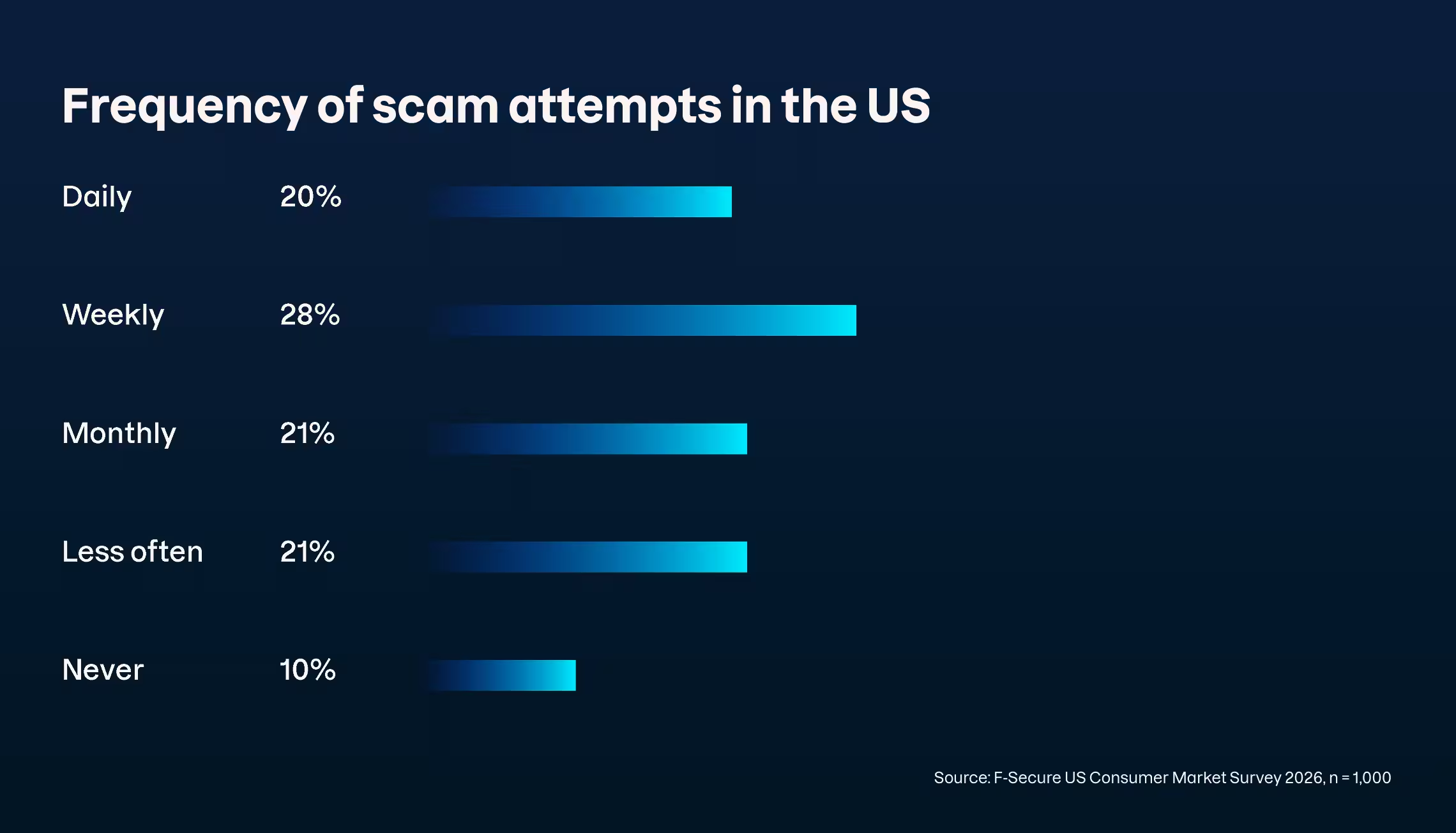

That baseline hasn’t changed. Over two thirds (69%) still encounter scam attempts monthly, and almost half (48%) face them weekly. At first glance, the landscape appears stable. But with 90% encountering at least one scam attempt last year, exposure has become nearly universal.

More than a third of consumers (37%) believe scam attempts increased compared to the previous year, even though measured frequency hasn’t drastically shifted for most age groups. This perception gap suggests that the experience of scams may be intensifying — even if frequency remains stable. But stable frequency doesn’t mean stable impact.

What stands out this year isn’t the number of scams, but how effectively cyber criminals are turning attempts into real financial harm. In this chapter, we examine what this evolution means for US consumers and the digital service providers they trust.

On This Page

In the United States, nearly half of consumers (48%) encounter scam attempts weekly, and 69% report monthly exposure — the highest levels recorded in our global survey.

Email remains the most common channel for scams, yet two in five attempts occur elsewhere, revealing a fragmented threat surface.

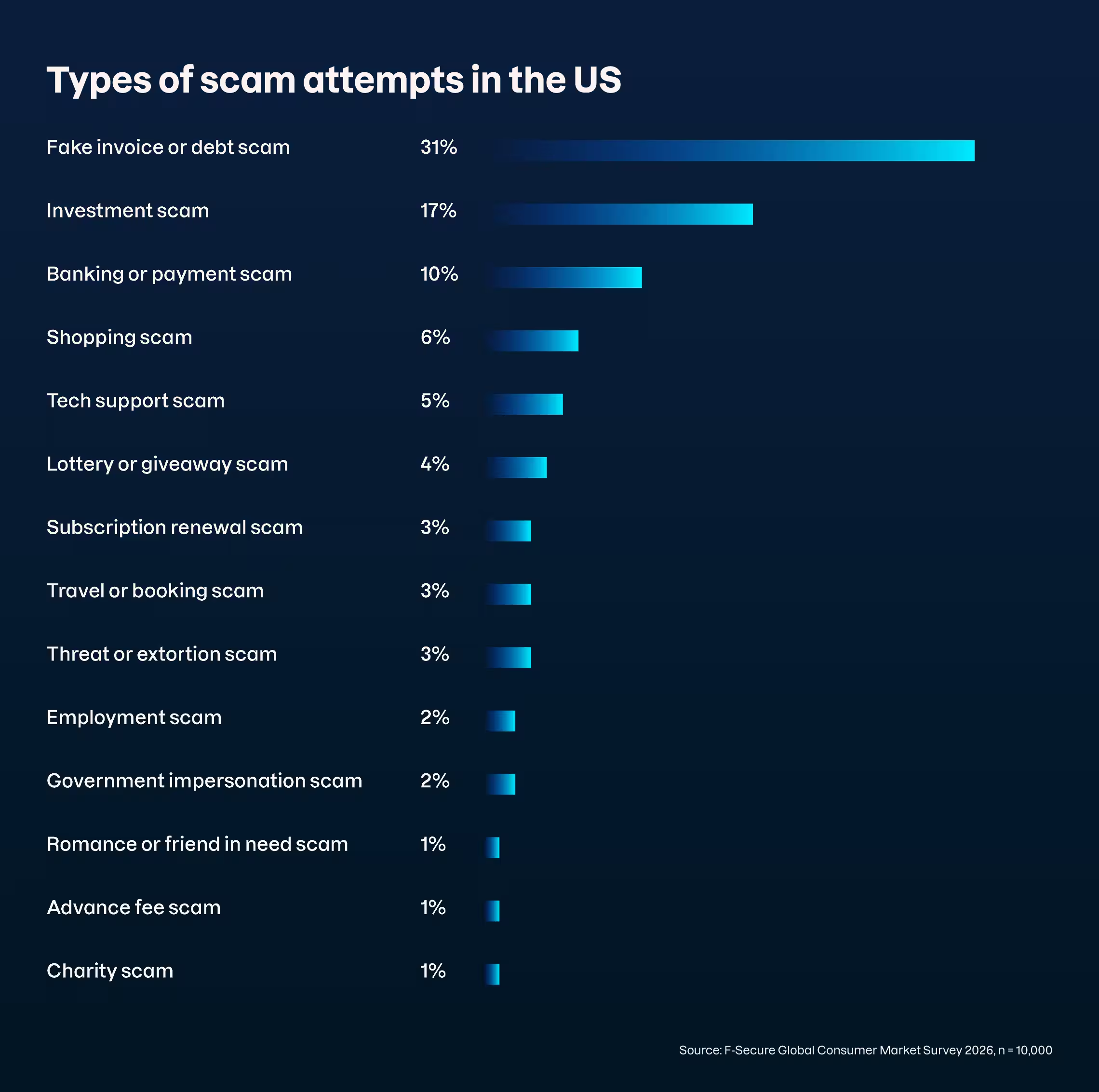

The most common scam attempts in 2026 aim to get money from victims directly. Fake invoice or debt scams (31%), investment scams (17%), and banking or payment scams (10%) now dominate the landscape — signaling a shift toward faster, higher-yield returns.

Scam exposure is widespread — but it’s also persistent. While 90% of US respondents encountered scam attempts last year, 15% of those exposed fell victim. That equates to around one in seven Americans falling victim overall, showing that scam victimization is common, not an exception.

In the United States, scam attempts and victimization are less closely aligned than global trends. High-volume scams such as fake invoice or debt fraud dominate in scale but convert at lower rates, while banking or payment and shopping scams generate a disproportionate share of victims.

The financial impact of scams surged over the past year. While 17% of victims reported losing money in 2025, that figure has more than tripled to 57% in 2026.

Consumer concern about future scams in the United States is high, with nearly half of respondents (47%) believing they are likely to fall victim. Willingness to pay for scam protection is similarly strong: 48% of Americans say they would pay for protection.

The findings across this report signal a structural shift. Scam exposure is still high, but financial harm is escalating — more than half of victims now lose money. At the same time, the demand for protection is strong. Nearly half of American respondents are willing to pay for scam protection, particularly younger, digitally active users.

Scam Exposure Remains High

In the United States, nearly half of consumers (48%) encounter scam attempts weekly, and 69% report monthly exposure — the highest levels recorded in our global survey.

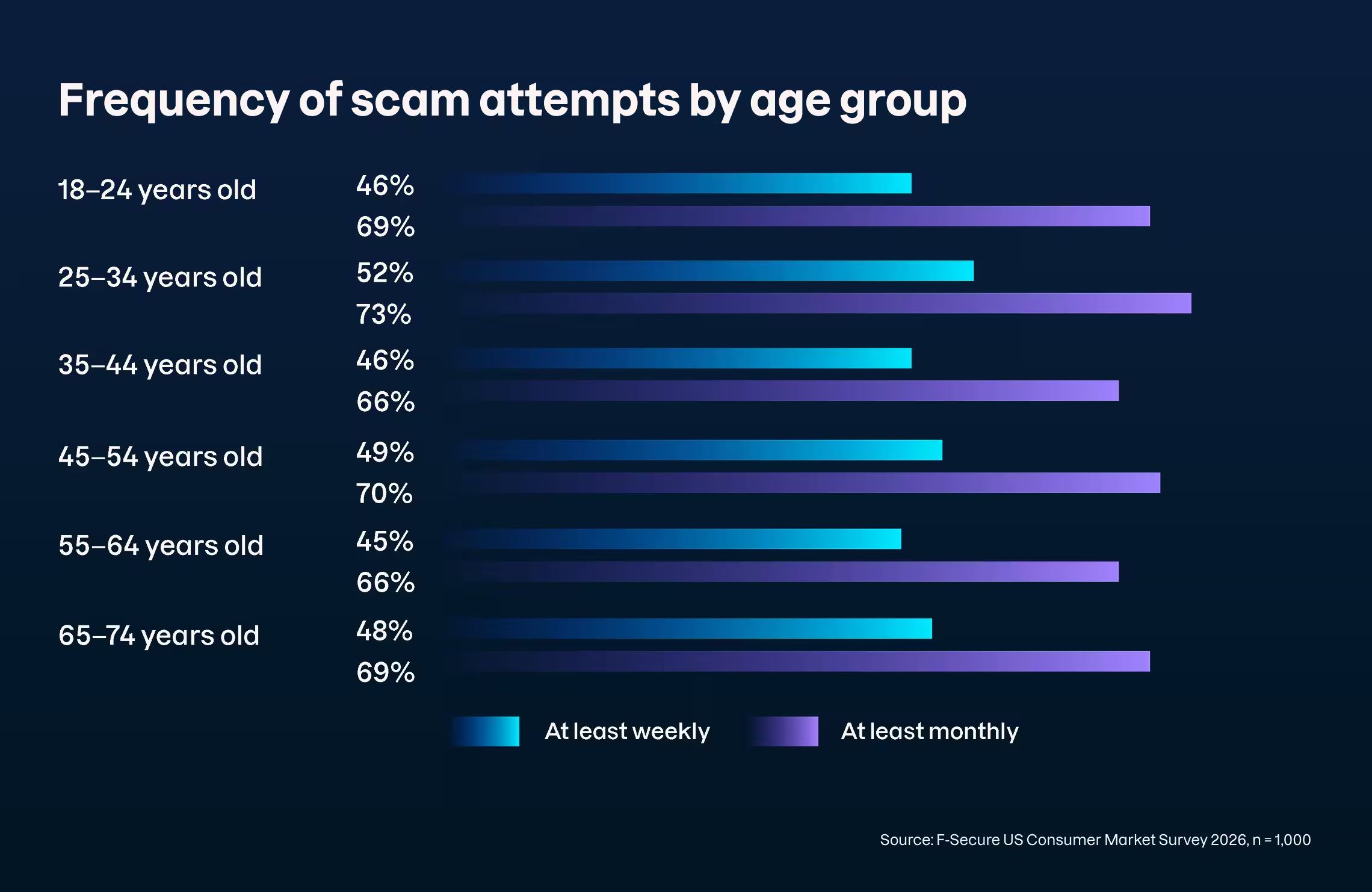

Unlike global trends, scam exposure in the United States isn’t concentrated among the most digitally active. It remains consistently high across all age groups, with both 18–24-year-olds and 65–74-year-olds encountering scams at nearly identical rates.

This points to a mature threat environment where risk is broadly distributed. Rather than focusing on a single high-risk segment, protection in the US must be built in by default — because scam exposure is the norm, regardless of age.

Scam Exposure is Multi-Channel, Not Just Email

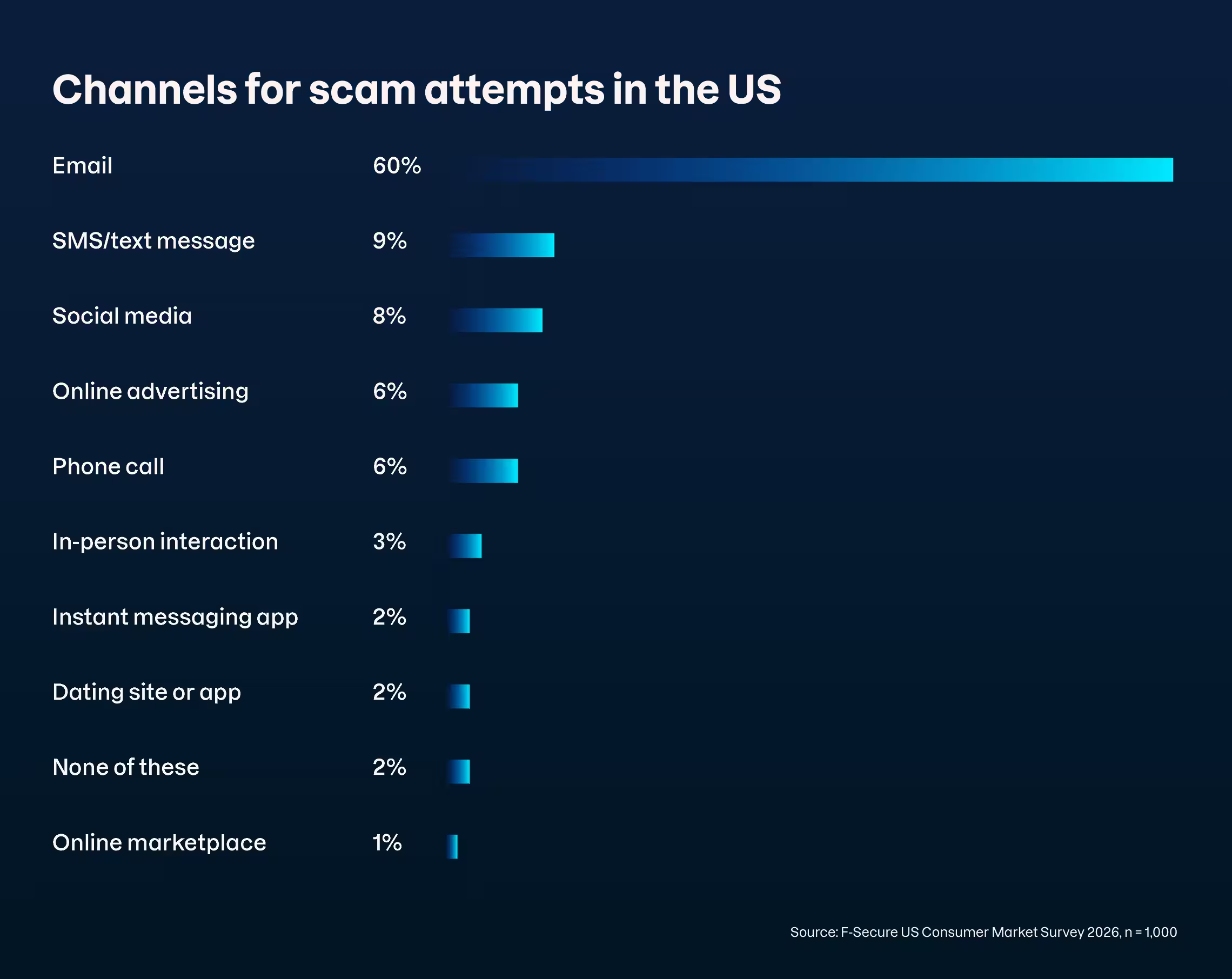

Email remains the most common channel for scams, yet two in five attempts occur elsewhere, revealing a fragmented threat surface.

Channel distribution also reflects generational behavior. Among 18–24-year-olds, exposure is spread across email (41%), SMS (13%), social media (13%), and online advertising (12%). In contrast, 65–74-year-olds face a more concentrated threat environment, with email accounting for more than three quarters (77%) of all attempts.

These figures reflect reported scam attempts and may not capture all exposure across channels such as social media and online advertising, where users may encounter suspicious content without directly engaging with it.

In the US, risk is widespread, but the channels used vary — particularly for younger generations — making effective protection inherently multi-channel.

Scams Are Optimizing for Higher-Value Returns

The most common scam attempts in 2026 aim to get money from victims directly. Fake invoice or debt scams (31%), investment scams (17%), and banking or payment scams (10%) now dominate the landscape — signaling a shift toward faster, higher-yield returns.

Year-over-year changes reinforce the evolution of the scam economy. Fake invoice scams have almost quadrupled since 2025 (8% to 31%), while banking and payment scams have doubled (5% to 10%). Investment scams have also increased, rising from 12% to 17%.

Meanwhile, shopping scams have fallen sharply (19% to 6%), suggesting either a shift away from consumer purchase-based scam models or stronger protections that prevent fake shops from reaching victims. The pattern points to a growing emphasis on scams that prompt victims to send money directly, rather than those disguised as online purchases.

Scam Exposure is Translating into Real Victimization

Scam exposure is widespread — but it’s also persistent. While 90% of US respondents encountered scam attempts last year, 15% of those exposed fell victim. That equates to around one in seven Americans falling victim overall, showing that scam victimization is common, not an exception.

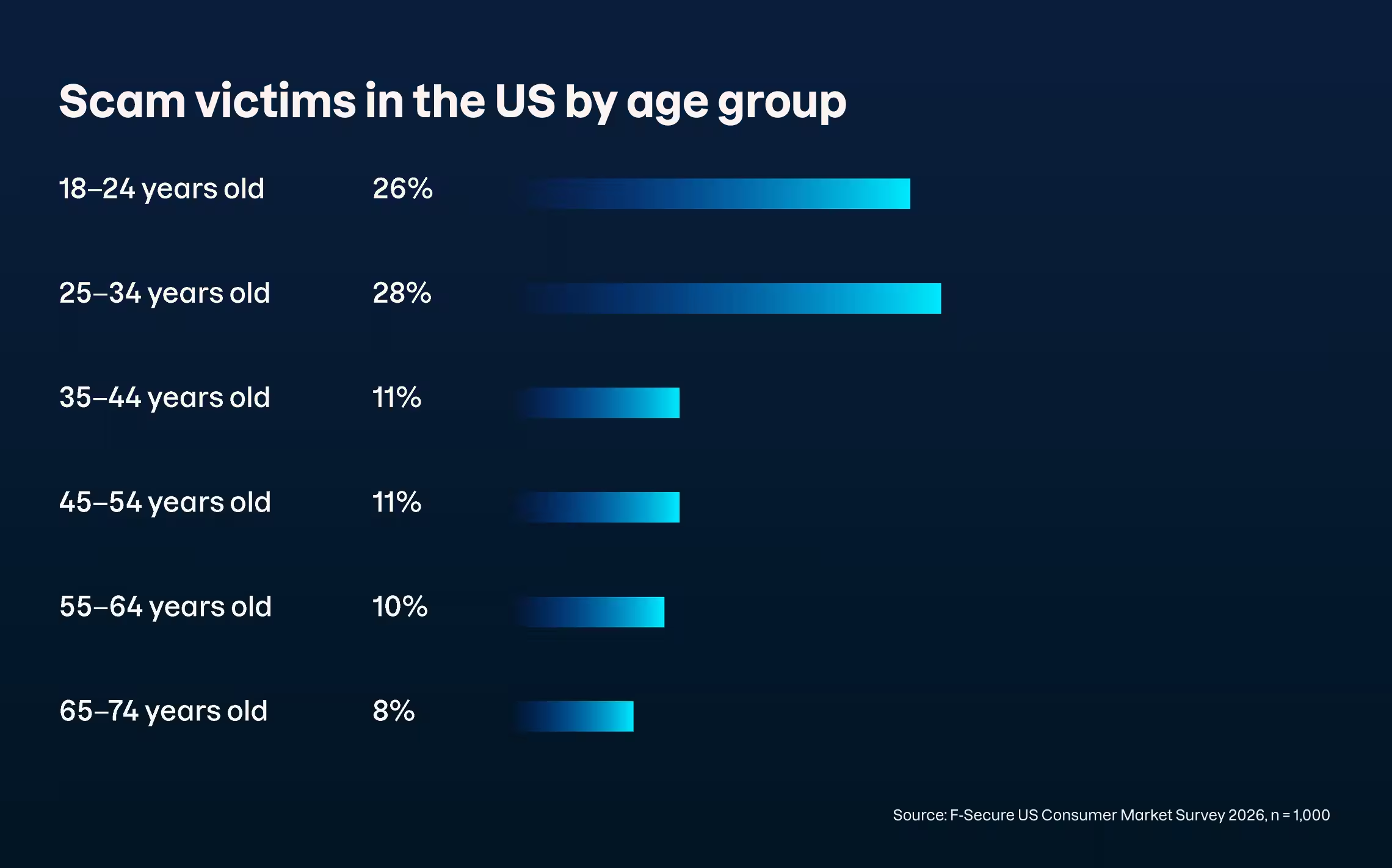

Age is also a defining factor. Younger adults are more than three times more likely to report having fallen victim to a scam, with 26% of 18–24-year-olds and 28% of 25–34-year-olds affected, compared to just 8% of those aged 65–74. Victimization declines with age, reinforcing how higher digital activity and multi-channel exposure increase risk.

However, age only tells part of the story. Even among those who believe they can recognize scams, 13% fall victim — compared to 24% of those who admit they can’t. In the scam economy, confidence alone is not enough.

The Most Common Scams Aren’t the Most Successful

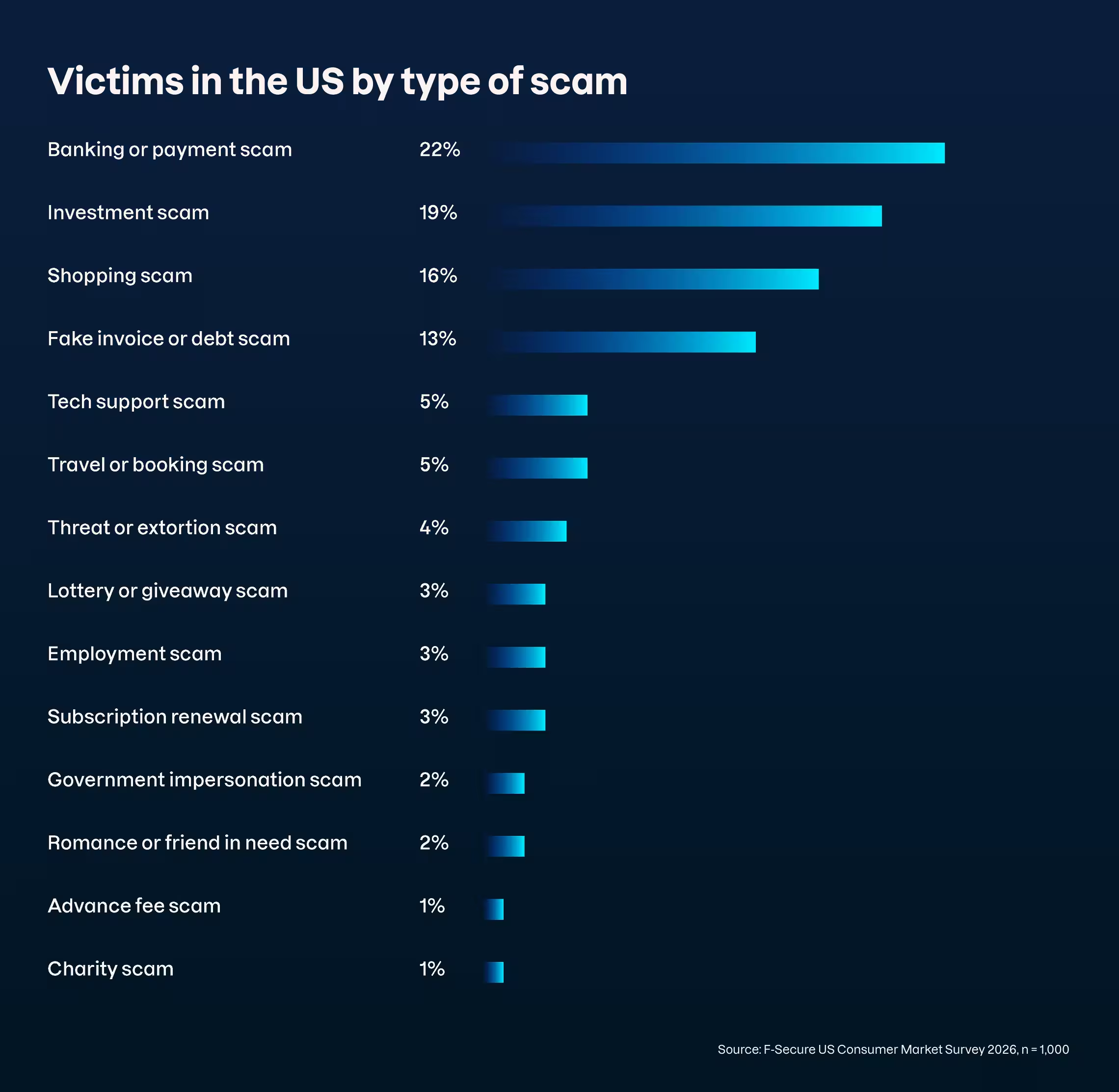

In the United States, scam attempts and victimization are less closely aligned than global trends. High-volume scams such as fake invoice or debt fraud dominate in scale but convert at lower rates, while banking or payment and shopping scams generate a disproportionate share of victims.

As a result, banking or payment scams (22%) account for more than one in five victims — making them the most successful scam model overall. Investment (19%) and shopping scams (16%) generate the second- and third-largest shares of victims, reinforcing that higher-value and transaction-driven scams are the most effective.

This shows that scam success in the US is driven not just by reach, but by the ability to exploit trust and moments of transaction.

More Than Half of Scam Victims Now Lose Money

The financial impact of scams surged over the past year. While 17% of victims reported losing money in 2025, that figure has more than tripled to 57% in 2026.

Financial loss is now the most common consequence of scams, far exceeding other impacts such as loss of personal information (16%), time (10%), and data (7%), as well as stress (5%) and reputational damage (1%). Only 5% said the experience had no significant impact.

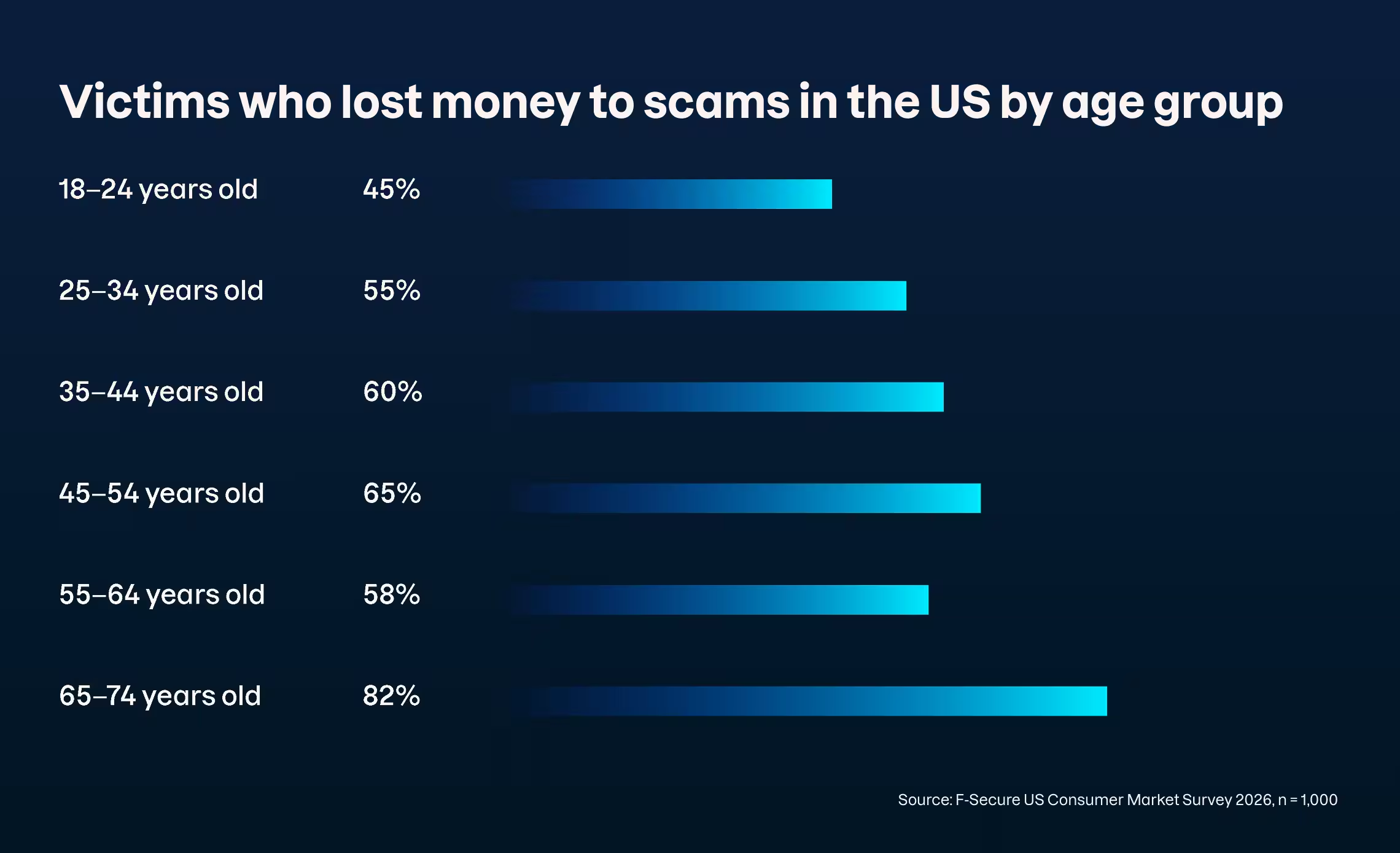

Age also reveals a distinct pattern. While younger adults fall victim more often, older adults are more likely to lose money once targeted. Among victims aged 65–74, 82% reported financial loss — the highest of any age group.

This shows that financial risk isn’t concentrated in a single demographic. Instead, it’s distributed differently: younger consumers are more likely to fall victim, while older consumers are more likely to suffer financial loss, pointing to the need for protection strategies that address both exposure and impact.

Demand for Scam Protection Remains Strong

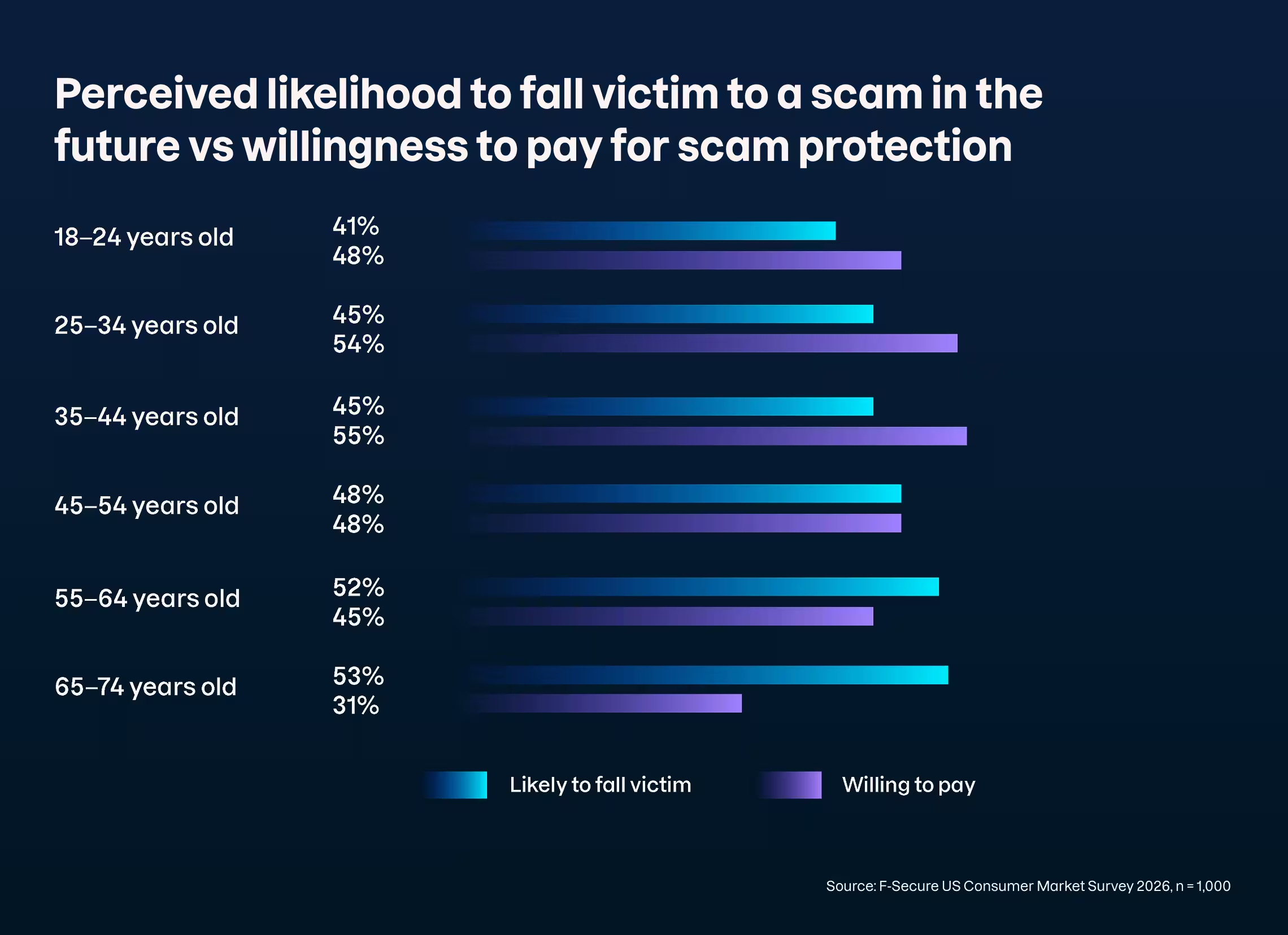

Consumer concern about future scams in the United States is high, with nearly half of respondents (47%) believing they are likely to fall victim. Willingness to pay for scam protection is similarly strong: 48% of Americans say they would pay for protection.

Exposure to scam attempts is consistently high across all age groups, but willingness to pay varies considerably. Younger adults are the most willing to pay for scam protection, reflecting their higher rates of victimization.

Perceived likelihood of becoming a scam victim, however, increases with age. More than half (53%) of 65–74-year-olds believe they are likely to fall victim in the future, compared to 41% of 18–24-year-olds. Yet willingness to pay moves in the opposite direction, falling to just 31% among the oldest age group.

Older adults show the lowest willingness to pay despite higher perceived future risk and greater financial losses when scams succeed. This highlights a disconnect between perceived vulnerability, potential harm, and demand for protection.

Strategic Priorities for Digital Service Providers

The findings across this report signal a structural shift. Scam exposure is still high, but financial harm is escalating — more than half of victims now lose money. At the same time, the demand for protection is strong. Nearly half of American respondents are willing to pay for scam protection, particularly younger, digitally active users.

The commercial implications of this shift are significant: 93% of US consumers say it’s important that their telecommunications provider offers cyber security, 82% say security influences provider choice, and 64% would switch providers based on their security offering. Scam protection is no longer an add-on; it’s a competitive differentiator.

Our 2026 findings define five strategic priorities crucial for digital service providers:

1. Cover the full digital journey

Scam exposure spans email, SMS, social media, mobile apps, and online advertising. Protection must extend across all digital touchpoints customers use every day.

2. Act in real time, not retrospectively

Financial harm occurs at the end of the scam journey, but engagement begins upstream in messaging channels. Providers must detect and disrupt scams as they happen, before they escalate.

3. Segment by risk profile

Younger consumers drive higher victimization, while older consumers experience greater financial severity once targeted. Providers should differentiate protection strategies between segments who fall for more scams and segments at higher risk of financial loss.

4. Make protection a core service, not an add-on

As scams become more targeted and financially damaging, security can't be treated as optional. It should be delivered as a baseline expectation, seamlessly integrated into the customer experience.

5. Lead with trusted relationships

Consumers look to their digital service providers for protection. Position security as a natural extension of that existing trust — strengthening engagement, loyalty, and long-term value.

Methodology

Consumer data was gathered via an online F‑Secure Consumer Market Survey conducted in January 2026. While self-reported data reflects individual perception, results were validated through sample balancing to ensure demographic consistency.

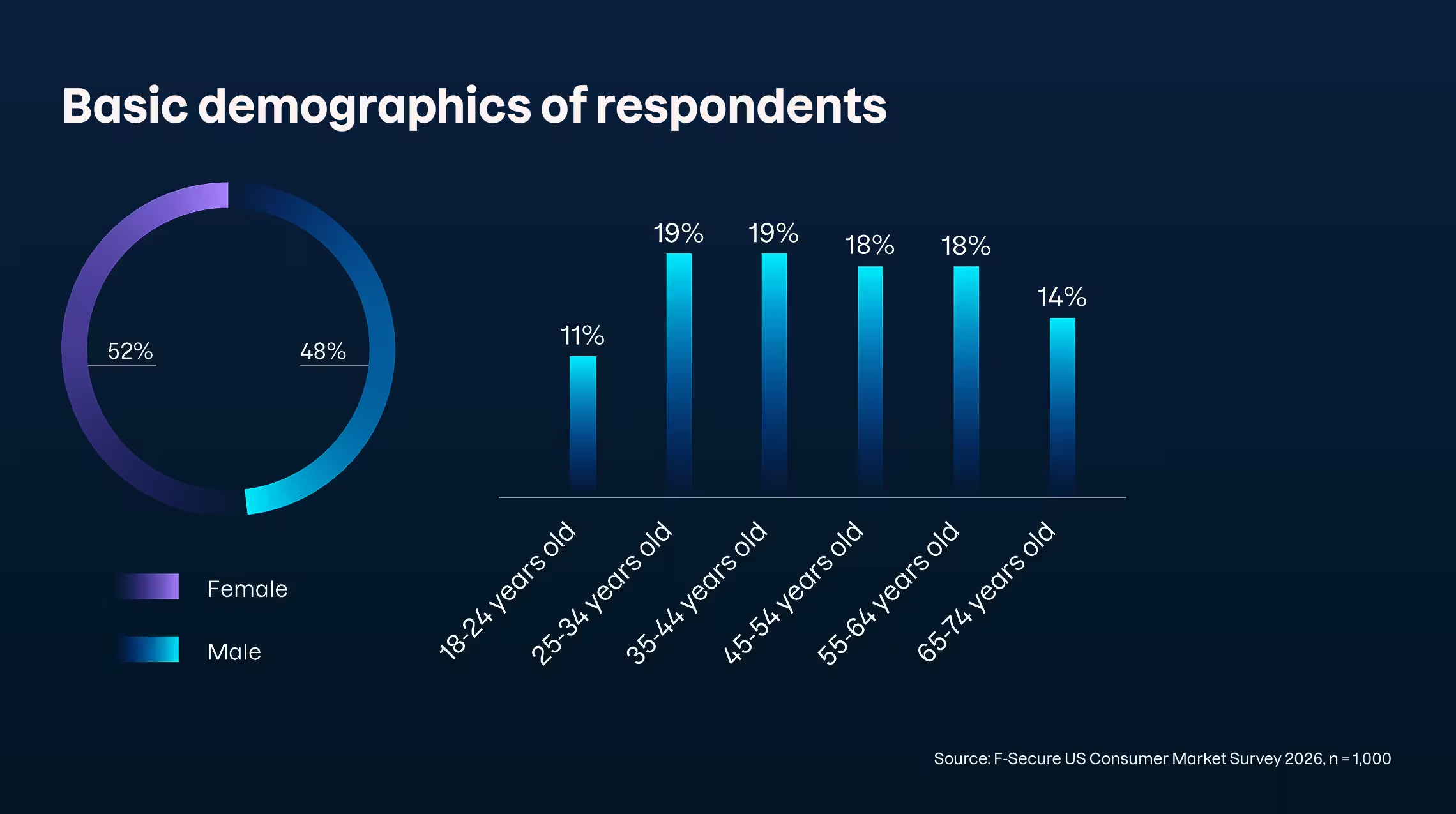

The survey captured responses from 1,000 consumers across the United States. Respondents ranged in age from 18 to 74, allowing for generational comparison in digital habits, and included a 52/48 gender split to reflect real-world diversity.